Three years ago, Sequoia partner David Cahn was one of the first people to crunch the numbers and calculate the implications of Silicon Valley’s titanic spending on AI infrastructure. In 2023, it was reacting to Nvidia’s annual GPU revenue of $50 billion. From that figure, and adding the implicit costs of operating the data centers

Three years ago, Sequoia partner David Cahn was one of the first people to crunch the numbers and calculate the implications of Silicon Valley’s titanic spending on AI infrastructure.

In 2023, it was reacting to Nvidia’s annual GPU revenue of $50 billion. From that figure, and adding the implicit costs of operating the data centers and the margins for their operators, he deduced that $200 billion in revenue would be needed to repay the initial investment.

He took it as a challenge and asked entrepreneurs to come up with AI products and services to use all that infrastructure and generate revenue from it. Fast forward to today, adding three years of hyperscaling, and Cahn has a new figure for AI infrastructure spending by 2026: $1.5 trillion.

In total, he estimates the AI industry will have to make $3 trillion to justify all those chips and other data center spending. And this is probably an underestimate: rising memory costs and the increasing use of exotic or inference-specific chips will increase that number. “Recently,” he writes, “required revenue per GW from CapEx has increased considerably due to this bottleneck dynamic and rising construction costs.”

On the other side of the ledger, Anthropic is believed to have hit $60 billion in ARR, while OpenAI reportedly made $13 billion in 2025 (although in November 2025, it said it was at $20 billion ARR) and is presumably making more this year. But it is clear that there remains a large gap to close.

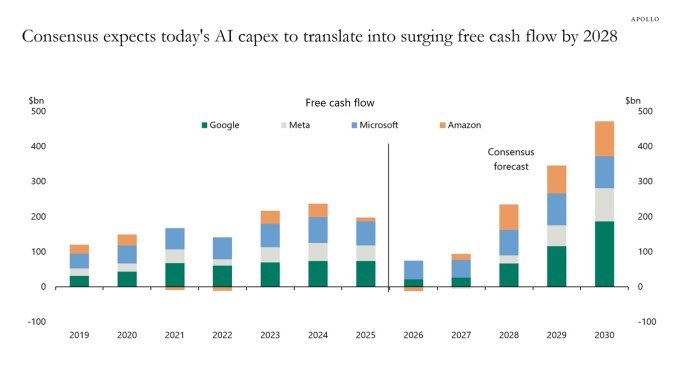

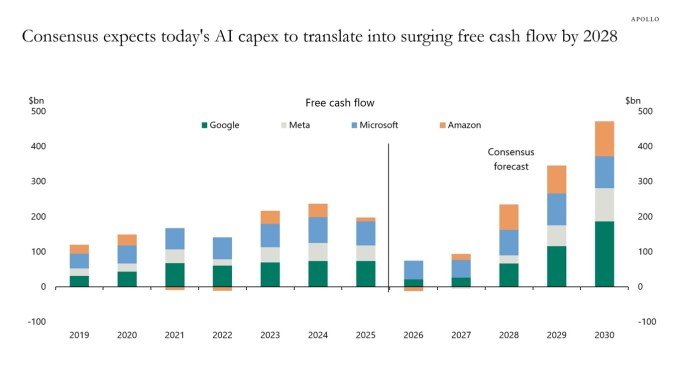

Someone addressing that gap is Torsten Slok, the chief economist at Apollo, the asset management giant. In a recent note, he points out that the hyperscalers (Google, Meta, Microsoft and Amazon) predict massive accelerations in their free cash flow in 2028. That is, they expect to see the return of all those chips they bought.

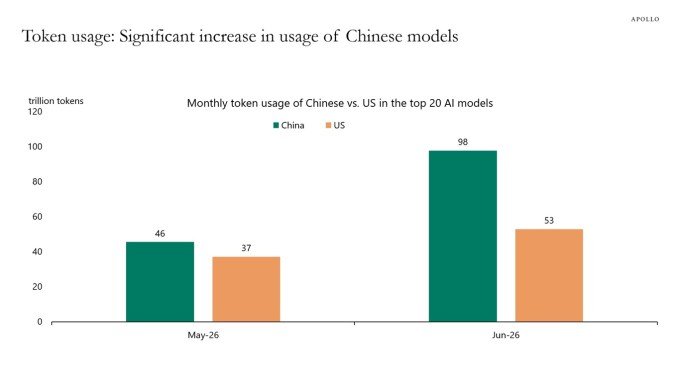

What happens if they don’t? Slok points out a risk we are currently seeing in the use of AI: more organizations turn to cheaper open models, often Chinese ones, not those built by frontier labs, and overall token prices fall. OpenAI’s latest model, according to CEO Sam Altman, is 54% more symbolic efficient at coding tasks. That’s good for users who care about the cost of their AI agents, but it can be bad for companies building token factories if users don’t massively increase their overall token usage with them.

Slok worries that if hyperscalers don’t meet their cash flow targets, the market reaction could be severe.

“With so much riding on so few names,” he writes, “slower returns would not just be a sector issue, but would risk sending the economy into a recession and the S&P 500 into a correction.”

There is just one thing you need to keep in mind while directing your AI agents towards cheaper tokens.

When you buy through links in our articles, we may earn a small commission. This does not affect our editorial independence.

Keep following us for the latest insights.