The stock market’s performance in the second quarter was historic on many levels. Major US indices posted their best returns since 2020. Semiconductors had their best quarter ever. But beneath the surface of the seemingly robust AI trade lurks a worrying divergence, a divergence that still has Wall Street strategists on edge. As chipmakers have

The stock market’s performance in the second quarter was historic on many levels. Major US indices posted their best returns since 2020. Semiconductors had their best quarter ever.

But beneath the surface of the seemingly robust AI trade lurks a worrying divergence, a divergence that still has Wall Street strategists on edge.

As chipmakers have exploded, hyperscalers have taken a backseat. The supposedly elite stocks of the Magnificent 7 have been surprisingly weak.

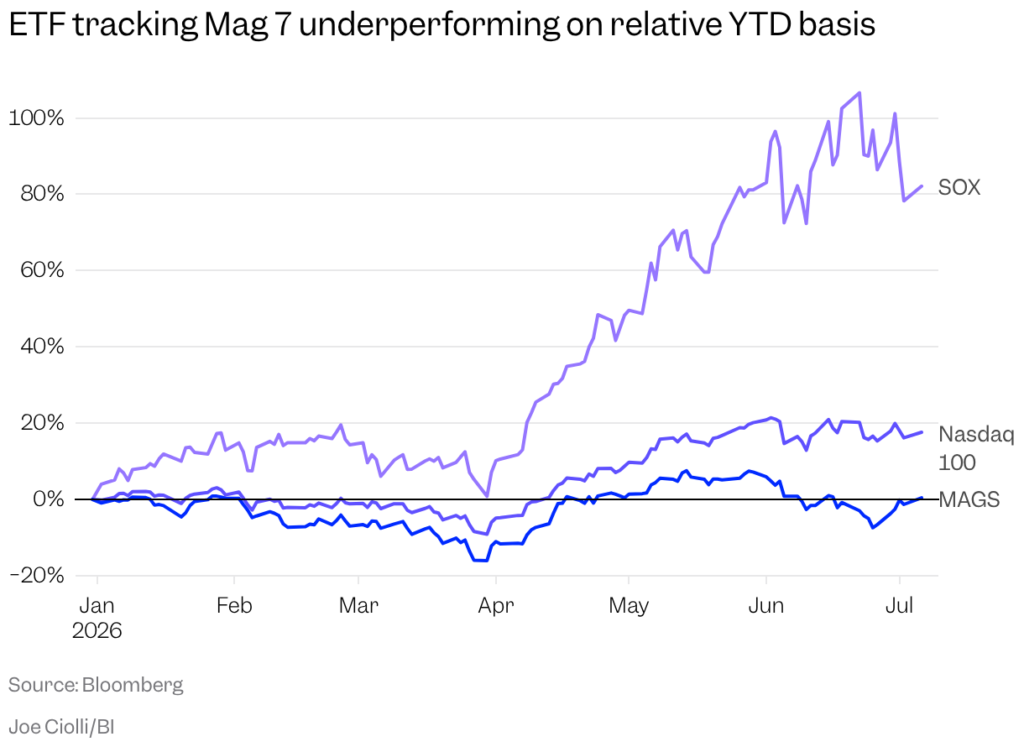

Forget the Mag 7: it’s been the Lag 7. The poor performance of the last few months is particularly evident when analyzed in graphs:

Investors have made it clear that they currently prefer companies that actually make the chips needed to drive AI commerce. Meanwhile, hyperscalers’ exorbitant capital spending has fallen out of fashion as operators increasingly question whether the investments will pay off. It’s a classic tug-of-war that has long defined AI trading.

Whether hyperscalers can close the gap is ultimately the question that will dictate how the entire AI trade fares through the end of 2026.

Wall Street’s top stock strategists are hopeful. The idea of a hyperscaler comeback keeps coming up in mid-year reviews and interviews.

Mike Wilson, Morgan Stanley’s CIO and chief U.S. equity strategist, is the latest prominent member of Wall Street to support the idea. He wrote in a note to a new client that he expects a rotation toward hyperscalers, away from chipmakers.

“Semiconductor stocks are going to correct,” he told Bloomberg TV, adding: “This divergence cannot be allowed to continue. It is not sustainable.”

Meanwhile, Ben Snider, chief US equity strategist at Goldman Sachs, recently told BI that resilient spending, combined with valuations that now look attractive, make hyperscalers a great investment option.

To round out Wall Street believers, JPMorgan recently laid out how the divergence between semi and hyperscaler could end up narrowing. In this scenario, hyperscalers improve monetization and start generating revenue and profits that allow them to capture a larger share of the AI pie.

This all sounds good. But is it easier said than done?

The upcoming Mag 7 earnings season, due in a couple of weeks, will offer the next critical litmus test on how investors feel about spending on AI and whether tangible results are coming fast enough.