Goldman Sachs says one of the market’s hottest trades is entering a new phase and investors may not be ready to take advantage of it. In a note, Goldman analyst Guillaume Jaisson examined the HALO trade, a term coined by Ritholtz Wealth Management CEO Josh Brown, which is short for “asset heavy, low obsolescence” and

Goldman Sachs says one of the market’s hottest trades is entering a new phase and investors may not be ready to take advantage of it.

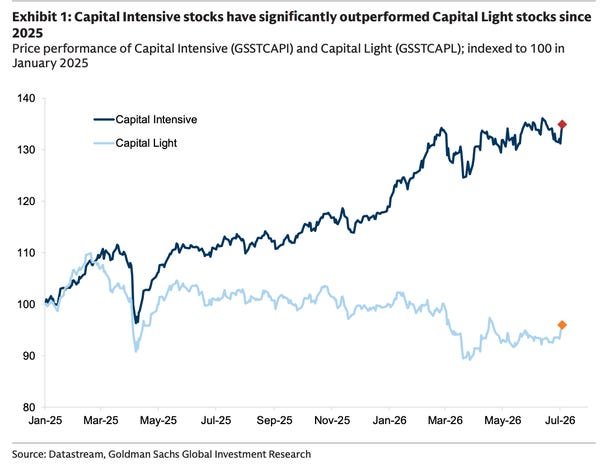

In a note, Goldman analyst Guillaume Jaisson examined the HALO trade, a term coined by Ritholtz Wealth Management CEO Josh Brown, which is short for “asset heavy, low obsolescence” and describes capital-intensive companies that own a large amount of physical assets. In a note to investors on July 7, he laid out the opportunity he sees as HALO trading enters its next phase of growth.

“Tactical positioning risks exist after a strong rally and HALO’s increasing correlation with the Momentum factor,” Jaisson wrote. “However, long-term allocations remain significantly skewed to value, suggesting investors remain underpositioned for a world in which physical assets, infrastructure and industrial capacity regain strategic importance.”

Goldman has been bullish on HALO trading for much of this year, as conditions shift from asset-light businesses such as software makers to asset-heavy companies in areas such as infrastructure, manufacturing and defense. It’s a trade that has endured through bouts of volatility caused by events like the Iran war.

“The outperformance has been strong and the shock ultimately reinforced our view,” Jaisson said. “Trading for the HALO pair, expressed as long Capital Intensive Companies (GSSTCAPI) versus short Capital Light Companies (GSSTCAPL), is up about 20% so far this year.”

Goldman Sachs

The analyst acknowledged the sell-off at the start of the Iran war, sparked by investors wanting to minimize exposure to companies exposed to global trade. However, the capital-intensive stocks at the heart of the HALO trade have since surpassed their pre-war levels and outperformed their capital-light peers.

Now his team sees a new phase of growth approaching, one that could provide even greater momentum for these companies in the near term.

“Capital Intensive shares have significantly outperformed Capital Light shares, driving substantial convergence in valuations,” he added. “Going forward, we expect profitability to become increasingly profit-driven.”

Jaisson noted that his team is now more confident in certain sectors such as energy security and industrial sovereignty. He added that Goldman stock analysts mostly agree, maintaining Buy ratings on half of the stocks in his team’s Capital Intensive basket.

Goldman pointed to a handful of sectors and stocks that are part of the HALO trade. They include: infrastructure (Enel, E.ON), Basic materials Materials (Shell, BP), Aerospace and Defense (Airbus, Rheinmetall) manufacturing and consumption platforms. (Volvo, BMW) and the physical layer of technology. (ASML Holding, ASM International).